|

|

|

CSULA Students Learn to Sniff Out Fraud In Accounting Class Sponsored/Taught by PCG Consultants By Rense, Kirk*

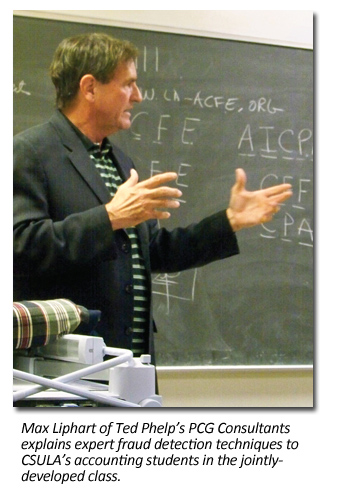

Ted has just added yet another facet to his interests professional and personal, however. This spring he and his staff have sponsored and are teaching a one-of-a-kind, case-based advanced forensic accounting class for California State University at Los Angeles’ outstanding Accounting Department. Officials at the school have worked closely with PCG Consultants to tailor the program to meet student needs. The University’s Accounting Department Chair Greg Kunkel had the idea for the class, and Dan Ryan, a CSULA professor and ATFE agent, spearheaded the development effort. Mr. Ryan, University Professor Kathryn Hansen, Ph.D., and PCG Consultants’ Max P. Liphart, Sarah Carson and Cindy Park spent a year preparing the course curriculum and materials, primarily underwritten by Ted Phelps’ PCG Consultants. Mr. Ryan, Mr. Liphart, Ms Carson and Ms Park are the principal instructors for the 12-week course. As an added bonus, an entire class devoted to computer forensics was taught by Manfred Hatzberger of the Pasadena firm Guidance Software, Inc. “This class offers students an inside look at how real fraud cases are investigated” said Mr. Liphart, a CPA and director of operations for Ted at PCG Consultants. “Students already get plenty of theory in other courses; this class uses actual cases and documents worked by PCG to teach the students how investigations are done in the nitty gritty world of forensic accounting and fraud investigations,“ Mr. Liphart added. Ted said he is delighted to be a part of such a valuable addition to the University’s curriculum: “We are extremely pleased to take part in this program and help educate the next generation of forensic accountants and investigators. Understanding the intricacies of fraud and embezzlement and how it is properly investigated is essential if accountants, fraud examiners and investigators are to adequately prevent and detect these crimes that cost American business billions of dollars each year,“ he said. Curriculum Students first explored the nature of a fraud engagement – goals and challenges – followed by discussion of a sample proposal and overview of the detailed planning necessary before undertaking an assignment. Real documents with redacted identifying information were then used to take students step-by-step through (a) how to locate pertinent documents, (b) how to detect early indications of intent to commit fraud in billing, shipping and accounting records, and (c) how to correlate companion or sequential documents to detect falsification of quantities and dollar amounts. “Knowing enough about the target business to identify the best persons to interview and most productive line of inquiry to follow takes time and planning,” Ted said. “The students learn that the scope of available materials and the type of apparent fraudulent scheme present shape the investigation and interviewing process.” Typical fraudulent schemes include manipulating accounts receivable aging (or re-invoicing older invoices), factoring schemes to over-qualify invoices for advances, or simply over-pricing goods on invoices to be factored. “The documents we use as examples from real cases (with identifying information redacted) are eye-openers of either how sophisticatedly or how crudely a fraud can be perpetrated,” Mr. Liphart said. “Sometimes it is almost comical, as when a draft invoice is found with a handwritten notation that all invoiced sums ‘need to be inflated.’ A $31,000 invoice can become a $96,000 invoice with a few keystrokes in an ethical vacuum,” he added. Kickbacks are another fertile area of investigation. Principal vendors are generally happy to receive substantial overpayments if allowed to retain a portion of the overpayment while returning the bulk of the amount under the table, Ted commented. “I like to think that PCG Consultants and I are doing our part in grooming the next generation of forensic accountants, and are giving a little back to the community at the same time,” he said. CSULA’s J. Gregory Kunkel, Chair of the Department of Accounting in the College of Business and Economics, praised the efforts of Ted Phelps and his team: “On behalf of the students and faculty of the Department of Accounting at California State University, Los Angeles, I want to thank you and your team of consultants for teaching our Case Studies in Forensic Accounting course. Your consultants were able to bring knowledge and real world experience to the classroom that was much appreciated by our students. Some of our best students remarked that it was the best accounting class they had ever taken at Cal State Los Angeles! “I know that your firm devoted a lot of time to make this class a success. Your willingness to give back to the Los Angeles community is exemplary. You and your team of PCG Consultants have had a positive impact on the lives and careers of the next generation of forensic accountants.” |

Ted

Phelps is a man with many interests quite apart from his successful Los

Angeles receivership practice PCG Consultants, which features special

expertise in forensic investigation. When not tracing and recovering

assets for financial institution clients or operating businesses as a

court-appointed receiver – most recently liquidating a string of auto

dealerships in Las Vegas under the aegis of the Clark County District

Court – Ted may be spending time at top dive spots around the world. From

Truk Lagoon to the Florida Keys, Ted might be the guy in the neoprene suit

next to you.

Ted

Phelps is a man with many interests quite apart from his successful Los

Angeles receivership practice PCG Consultants, which features special

expertise in forensic investigation. When not tracing and recovering

assets for financial institution clients or operating businesses as a

court-appointed receiver – most recently liquidating a string of auto

dealerships in Las Vegas under the aegis of the Clark County District

Court – Ted may be spending time at top dive spots around the world. From

Truk Lagoon to the Florida Keys, Ted might be the guy in the neoprene suit

next to you.